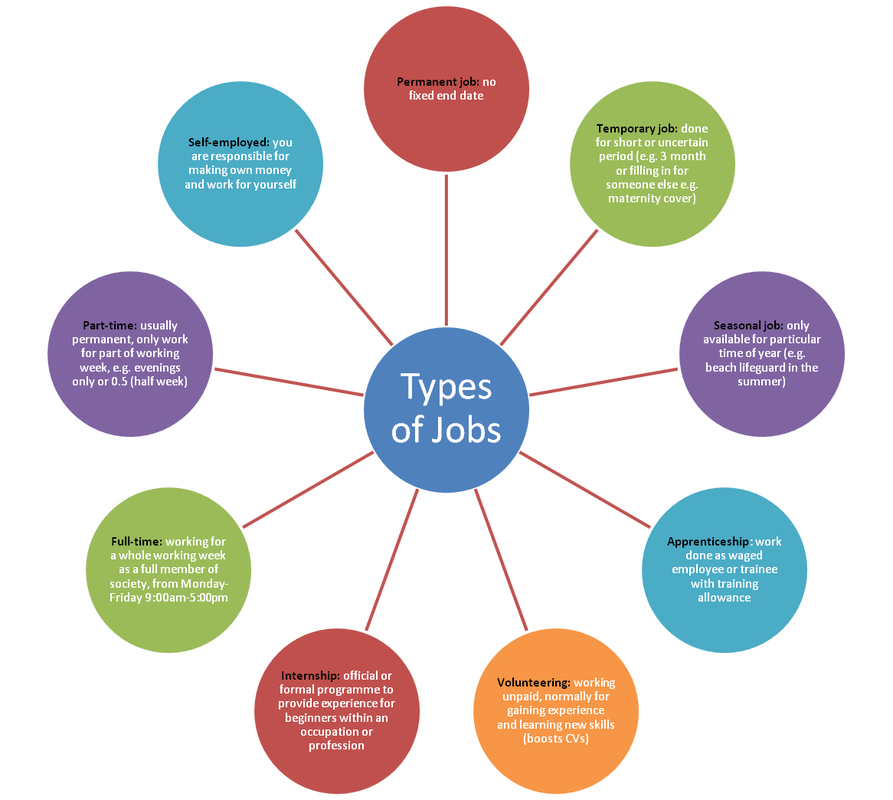

Income

There are many ways that individuals receive an income, the most common being through a wage. Different terms are used to describe various ways of working and types of jobs.

Getting Paid

When do I get paid? If you are working you are generally paid weekly or monthly. However if you are doing an Apprenticeship you will get a wage of at least £95 a week.

What will I get paid? As an employee your employers should provide you with a clear statement of what your pay. Or if you are a trainee you should be informed on what your training allowance is.

However regardless of what type of job you hold employers are permitted by law to pay their workers at least the set lowest wage. This in the UK is known as National Minimum Wage, and this minimum wage rate per hours is dependent on your age and whether you are an apprentice. The table highlights the current (2014) minimum wages;

What will I get paid? As an employee your employers should provide you with a clear statement of what your pay. Or if you are a trainee you should be informed on what your training allowance is.

However regardless of what type of job you hold employers are permitted by law to pay their workers at least the set lowest wage. This in the UK is known as National Minimum Wage, and this minimum wage rate per hours is dependent on your age and whether you are an apprentice. The table highlights the current (2014) minimum wages;

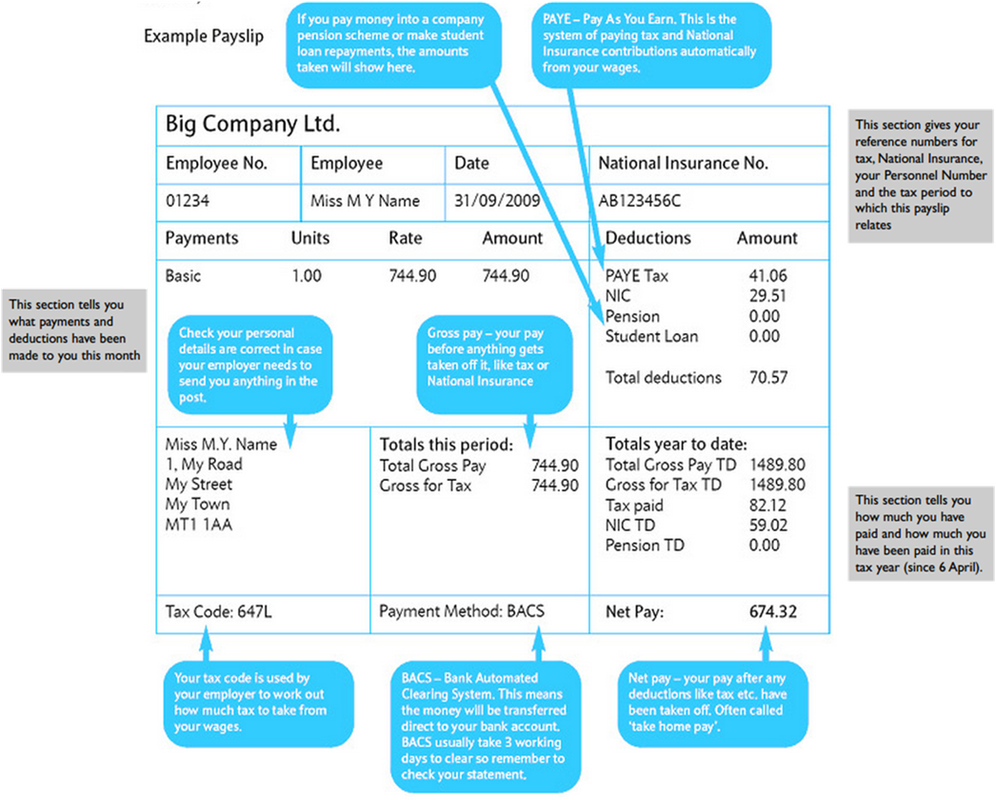

How you receive wages?

Some employers pay their employees either through cash or in a pay packet while others have their salary paid directly into their bank or building society account. Either way, as an employee you receive a payslip, which informs you about the total amount you have earned and how much of the amount you get to keep for personal use. You are advised to retain payslips for a minimum of a year, as you may need as a form of proof e.g. of your salary or tax paid.

Pay slip explained

National Insurance Number: everyone receive a national insurance number which is sent to them when they turn 16. The number is used for identification for work and training, or when claiming benefits. The number allows others to make sure that your National Insurance contributions and tax are only recorded against our name.

|

Pay deductions

The pay slip demonstrates how income is deducted; 1. Income tax:

2. National Insurance contribution

|

3. Pension scheme contributions

4. Student Loan Deductions

|

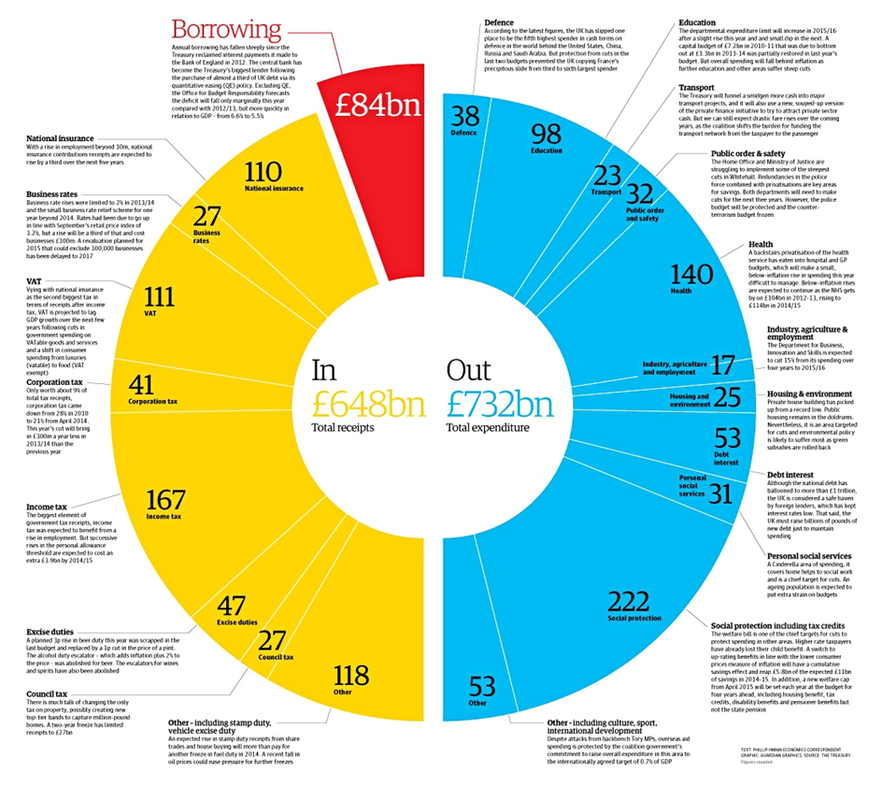

Why do you pay tax?

|

The Government raises funds by takes a percentage of your earning in the form of income tax to pay for may goods and services that they provide for their citizens. There are fifteen main government departments which rely on public money to function. Every year the government decides how much money will be spent on each department. The government budget can be seen in the image.

|

Where to put your money?

Bank and Building society accounts

There are two types of accounts: current accounts and saving accounts.

There are two thing you can do with your money when in a account;

Current Accounts

Current accounts are basic accounts for day-to-day transactions. You will receive a regular bank statement, typically once a month, to show transactions that have occurred in your account. For instance how much you have paid in, withdrawn and how much money you have available in the account otherwise known as balance. Your statement will also show how much interest your money has earned, however this is typically a small amount as current accounts offer low interest rates.

It is good practice to double check you bank statement to ensure all details are accurate. This means checking the withdrawals you have made or bills you have paid, 'debits' as well as money paid into your account 'credit'.

There are two types of accounts: current accounts and saving accounts.

There are two thing you can do with your money when in a account;

- You can pay in (deposit) money you receive e.g. wages or student loans

- You take out (withdraw) money, when you need to pay for things

Current Accounts

Current accounts are basic accounts for day-to-day transactions. You will receive a regular bank statement, typically once a month, to show transactions that have occurred in your account. For instance how much you have paid in, withdrawn and how much money you have available in the account otherwise known as balance. Your statement will also show how much interest your money has earned, however this is typically a small amount as current accounts offer low interest rates.

It is good practice to double check you bank statement to ensure all details are accurate. This means checking the withdrawals you have made or bills you have paid, 'debits' as well as money paid into your account 'credit'.

|

|

Every bank offers its customers a variety of accounts that presents different incentives and rates of interest. Some examples of current accounts include;

|

|

Saving Accounts

If you want to save money for purposes other than very short-term, a saving account with a bank or building society is better than a current account as it offers more interest. You can use saving accounts either to save regularly or save when you have some spare cash. A variety of saving accounts are offered to customers;

|

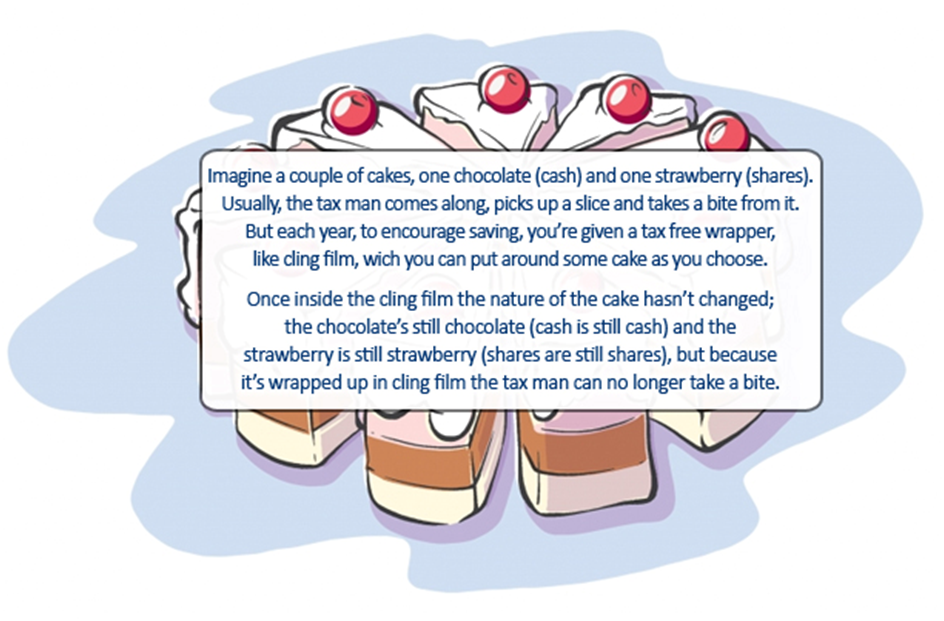

Explanation of how New ISAs work

|

Standing order and direct debit

If you wish to save the bother of paying regular bills the arrangements can be done for you by creating a standing order or direct debit

If you wish to save the bother of paying regular bills the arrangements can be done for you by creating a standing order or direct debit

- Standing order: instruction to your bank to make regular payments of a fixed amount. Either to someone else or to another account in your name e.g. saving account.

- Direct debit: an authority which you give to someone else to claim money from your bank account to meet your bills or repay your loans. E.g. telephone and gas bills are usually aid using this method.

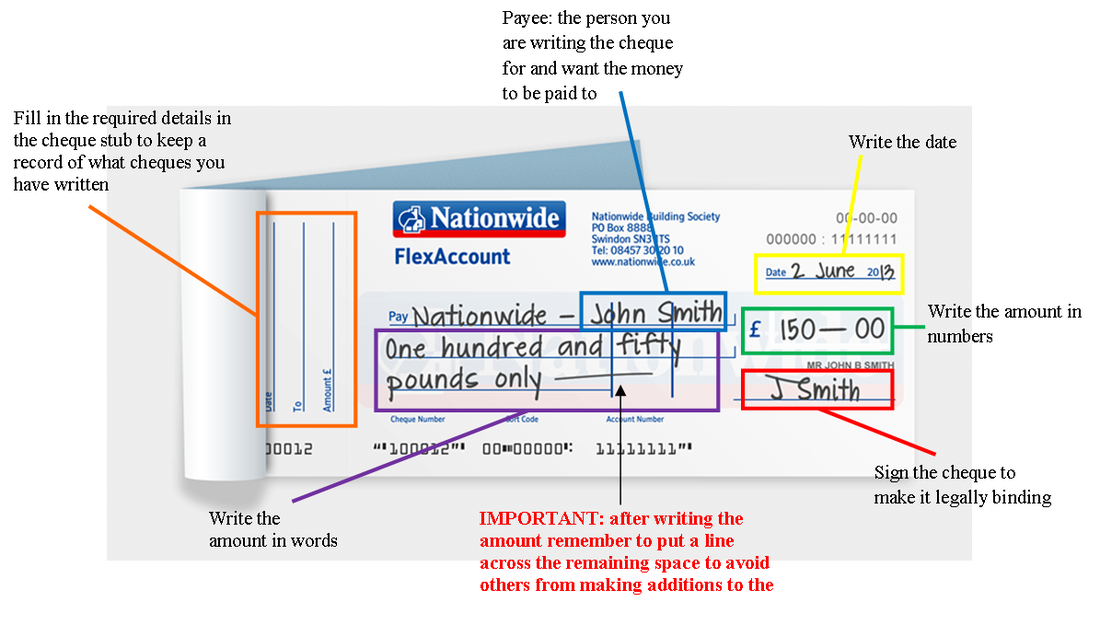

Cheques

Some banks issue their customers depending on their account with a cheque book. Below is an explanation about how to fill in cheques.

Some banks issue their customers depending on their account with a cheque book. Below is an explanation about how to fill in cheques.

If you receive a cheque, you have to take it into your bank to pay it into your bank account. After a few days the money is debited from the account of the person you received the cheque from and credited to your account.

IMPORTANT: remember that your signature binds you in law to whatever you have agreed to buy or borrow.

IMPORTANT: remember that your signature binds you in law to whatever you have agreed to buy or borrow.

Plastic Cards

As previously stated when you open an account in a bank you may be issued with a plastic card. There are different types of card and they all have varying function;

|

1. Cash Card

Allows you to get cash from cash machines using a PIN (personal identity number). You should ALWAYS keep your pin a secret; in the any case if you lose it or it is stolen you have to inform you bank immediately. 2. Debit Card (e.g. Maestro) Allows you to buy items without writing a cheque or carrying cash. Can also be used while purchasing items over the phone or on the internet. Can be thought of as a 'electronic cheque'. When it is used, the amount of your purchase is 'debited to' your account, usually 2 or 3 days after. The transaction will appear on your bank statement under the suppliers name. At certain places you are as well as buying goods you are able to withdraw cash from the till, known as 'cash back'. Most debit cards are also cash cards. 3. Credit Card (e.g. Visa, Mastercard) Also allows you to buy goods and services from any supplies in person or over the telephone or internet. On a credit card you pay for things now but you don't receive the bill till later. So the bank which issued you with a credit card is lending you money to for to use. When you open your credit card account you will be told your limit (how much money you can borrow). If you exceed this limit the card may be taken away from you. |

|

Just like other card, you will also receive a statement, outlining what you have spent using the card, every month. The statement also tell you how much you owe them and by what date you will need to make the repayment. You have the option to repay the bill in full or in instalments. If you choose to only pay off part of the outstanding bill you are usually charged interest on the whole balance, before deducting the payment. This can become a very expensive method of borrowing money and could if not kept up with can result in debts.

As stated above plastic cards can be very useful however they do all come with caution and danger signs because if they are not used unwisely you could run up large debts and interest charges.

As stated above plastic cards can be very useful however they do all come with caution and danger signs because if they are not used unwisely you could run up large debts and interest charges.

How to secure your card?

Every transaction made with a credit card can be traced, so it can be easy to prove id a payment has been made by you or someone else without your acknowledgement. If you money has been stolen without your knowledge most banks will pay you back, on the conditions that they know the problem immediately after you discover it.

Chip and Pin

This is the name given to a security method used with credit and debit cards. When paying in person you have to enter your PIN into a machine to ensure that the card is yours, only then will the transaction be processed.

Online shopping

Online shopping can be an easy way for people to steal your personal details. Therefore only ever buy items using a secure computer network and from a reputable company with a secure online purchasing service.

Chip and Pin

This is the name given to a security method used with credit and debit cards. When paying in person you have to enter your PIN into a machine to ensure that the card is yours, only then will the transaction be processed.

Online shopping

Online shopping can be an easy way for people to steal your personal details. Therefore only ever buy items using a secure computer network and from a reputable company with a secure online purchasing service.

Borrowing Money

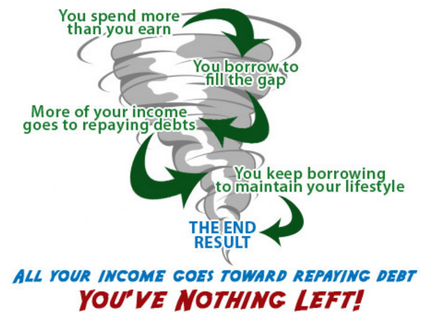

If you do not have the sufficient funds you are able to lend money from a bank or banking society through an overdraft or by loan. As explained previously stated credit cards allow you to borrow money in a easy and convenient way. However it can be expensive if you don't have the money to pay the bank off at the end of each month as you will be charged high rate of interest. People are advised not to borrow money using credit cards as it can get people into a vicious cycle of borrowing which results in massive amounts of debt.

|

Overdraft

An overdraft is where in the event that your balance is 0 you are able to borrow from the bank. However the bank will charge you for an overdraft facility through fees and interest. The most expensive overdraft is an unauthorised overdraft, where you are overdrafting money without the agreement or acknowledgement of your bank. It is the most expensive form of overdrafting as you pay heavy interest on the amount you have overdrafted, as well as the charges on top. If you are aware that you will be overdrafting on a regular basis you should arrange a authorised overdraft with your bank. However if you exceed the authorised overdraft you will be charged and heavily interests will be applied. There is still the potential for costs of interest and fees to mount, but they will be significantly less then unauthorised overdraft. Loan A loan can be arranged for your bank to lend you a specific amount of money. When agreeing to this loan the bank will outline a specific period for repayment and an agreed rate of interest. This form of borrowing money has lower risk of entering debt, as you can verify whether you can afford the repayments before agreeing to the loan. |

|

Budgeting & managing your money

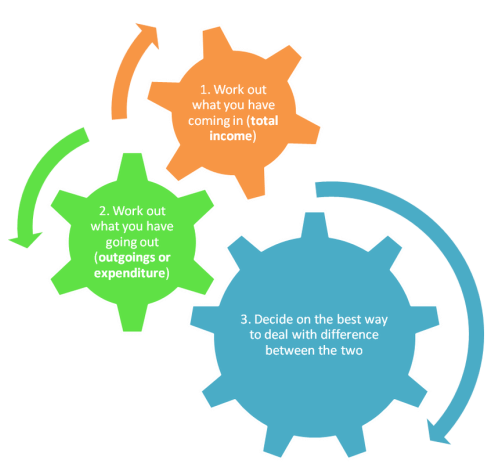

The best way to manage your money is to make a budget plan so you are aware how much money you have coming in and going out. This allows you to; avoid a bad debt situation and have a sense of what you can and cannot afford. There are three simple steps you can take to draw up a budget plan.

|

1. How much income?

Total income is accumulated from various places; wages or training grant, student grant and loan (only if you are a student), any state or other benefits which you receive and money which you get from your parents or others. 2. How much an I spending? You have to consider and include everything that you spend. By making a list of all the items you have spent money on you will know your non-discretionary expenditure. This includes travel to and from school, food and mobile phone. It is also important to remember to include the amount of your repayments as well as the interest you are paying. You also need to estimate what you will spend on non-essentials as this counts as discretionary expenditure. This includes things such as entertainment and other socialising, eating out, holidays, clothing and sporting activities. When completing this you need to be honest and realistic!!!! If you under-estimate what you are spending your financial situation may appear to be better than in reality. 3. Work out the Balance The final step is to determine what your balance is which is calculated by subtracting your expenditure from your income. If the number is positive (well done!) then you can consider whether you can put extra money aside into a savings account. However is it is a negative figure you are potentially heading towards debt by spending more than your income/ you have. You will have to reconsider you outgoings and whether you need to borrow money to control and keep up with your outgoings. |

Government Financial Aid

Some members within society are entitled to financial assistance from the government if they are struggling. The following section outlines the state benefits available to those who are unemployed and are struggling for income.

|

1. Jobseeker's Allowance (JSA)

This can be claimed if you fall within the following criteria:

2. Income Support This form of support is provided to those who are;

|

|

In these circumstances you are not expected to work or take a training place.

For those who are 18 and still unemployed the JSA and income support are available to you only if you are; capable of working, available for work and actively seeking work.

For those who are 18 and still unemployed the JSA and income support are available to you only if you are; capable of working, available for work and actively seeking work.

|

3. Housing benefit

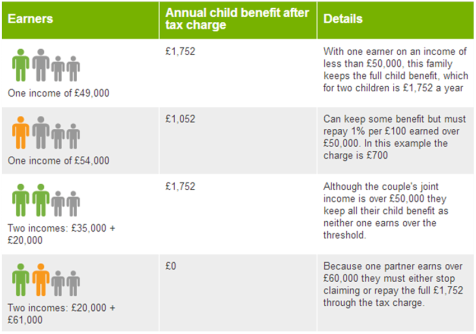

This benefit is run by the local council to whom you have to provide evidence with that you are unemployed and/or on low income. This type of benefit provides you with money to pay rent. 4. Child benefits This is a tax-free payment which is aims to help parents cope with the cost of bring up children. The amendments to the benefits has meant that while previously it was available to every family with children, now the amount you receive is dependent on the household income. |

Teaching Ideas

Starter:

Ask students to write down on post-it notes all the words they can think of that relates to money (this could also include currency).

Ask students to estimate the price of various items e.g. 1 loaf of bread, 1 months gas bill for 2 people and the cost of a full tank of petrol for a medium sized car

As a recap of previous lesson on bank accounts students will be given four different situations and they have to decide which account or method of saving would be best (ensuring students give a reason for their choice). The situations could be as followed:

Give students a list of things households may spend their money on e.g. food, take away, bus fare, stationary... They have to distinguish between necessities and luxury items.

Main task:

Students will be provided with four different profiles based on real people who found themselves in situations where they needed financial support from the government. Using a benefit information sheet or notes from the lesson students are required to work out which benefit they may be eligible for.

Provide students with a case study with information that students require to fill in a blank pay slip. (cross-curricular links to maths and business studies).

At the end of the topic to test students knowledge and skills you can set them a budget challenge (you could provide 4 different challenges and students can chose which one they prefer). One example of a challenge could be holiday saving. In this challenge students have to plan and cost an affordable holiday. They have to imagine that they and a friend have been give £200 each but there is a possibility for them to earn/save more over the next year before they go. The task requires students to research and record their findings which has to include; their destination, duration, cost including food and spending money. Also it the costing is more than £200 each how are they going to obtain the remaining money, showing their budget plan. At the end they have to give a presentation to the rest of the class.

Plenary:

Ask students to fill in a blank check. Different sources can be given to students which provides the information required to fill in the cheque e.g. a school letter asking for school trip payment or gas or electric bill that needs paying.

Ask students to write down on post-it notes all the words they can think of that relates to money (this could also include currency).

Ask students to estimate the price of various items e.g. 1 loaf of bread, 1 months gas bill for 2 people and the cost of a full tank of petrol for a medium sized car

As a recap of previous lesson on bank accounts students will be given four different situations and they have to decide which account or method of saving would be best (ensuring students give a reason for their choice). The situations could be as followed:

- A relative wins the lottery and gives you £1000

- You want to save for a special holiday after your exams

- You have a Saturday job and want to save a small amount regularly

- You are going to college and need a bank account

Give students a list of things households may spend their money on e.g. food, take away, bus fare, stationary... They have to distinguish between necessities and luxury items.

Main task:

Students will be provided with four different profiles based on real people who found themselves in situations where they needed financial support from the government. Using a benefit information sheet or notes from the lesson students are required to work out which benefit they may be eligible for.

Provide students with a case study with information that students require to fill in a blank pay slip. (cross-curricular links to maths and business studies).

At the end of the topic to test students knowledge and skills you can set them a budget challenge (you could provide 4 different challenges and students can chose which one they prefer). One example of a challenge could be holiday saving. In this challenge students have to plan and cost an affordable holiday. They have to imagine that they and a friend have been give £200 each but there is a possibility for them to earn/save more over the next year before they go. The task requires students to research and record their findings which has to include; their destination, duration, cost including food and spending money. Also it the costing is more than £200 each how are they going to obtain the remaining money, showing their budget plan. At the end they have to give a presentation to the rest of the class.

Plenary:

Ask students to fill in a blank check. Different sources can be given to students which provides the information required to fill in the cheque e.g. a school letter asking for school trip payment or gas or electric bill that needs paying.